Are you a homeowner looking to unlock the potential of your home’s equity? If so, you’ve likely come across two common options: Home Equity Lines of Credit (HELOCs) and Home Equity Loans.

Understanding the Basics

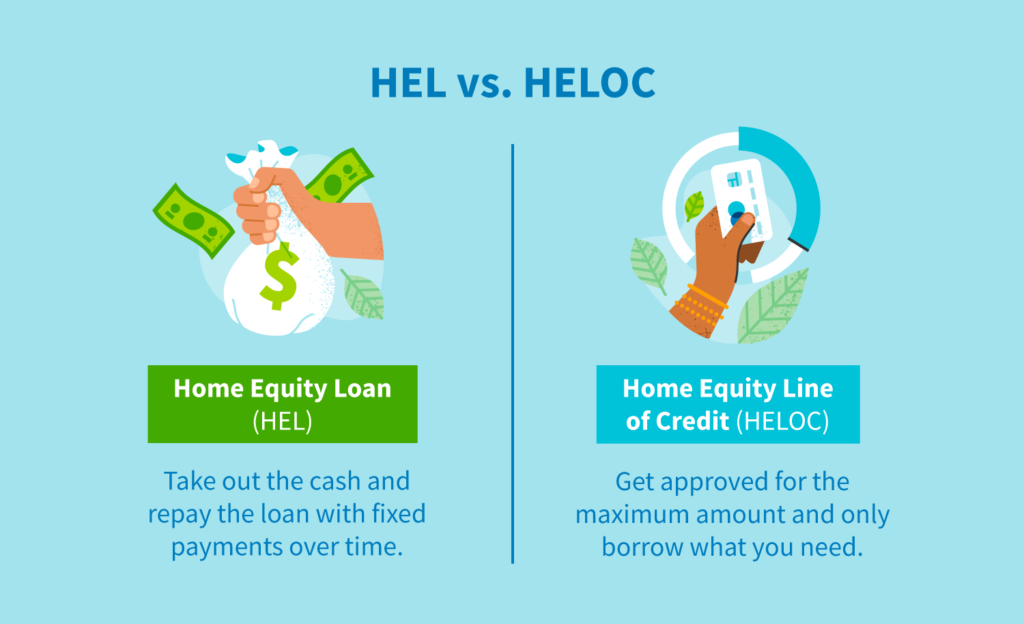

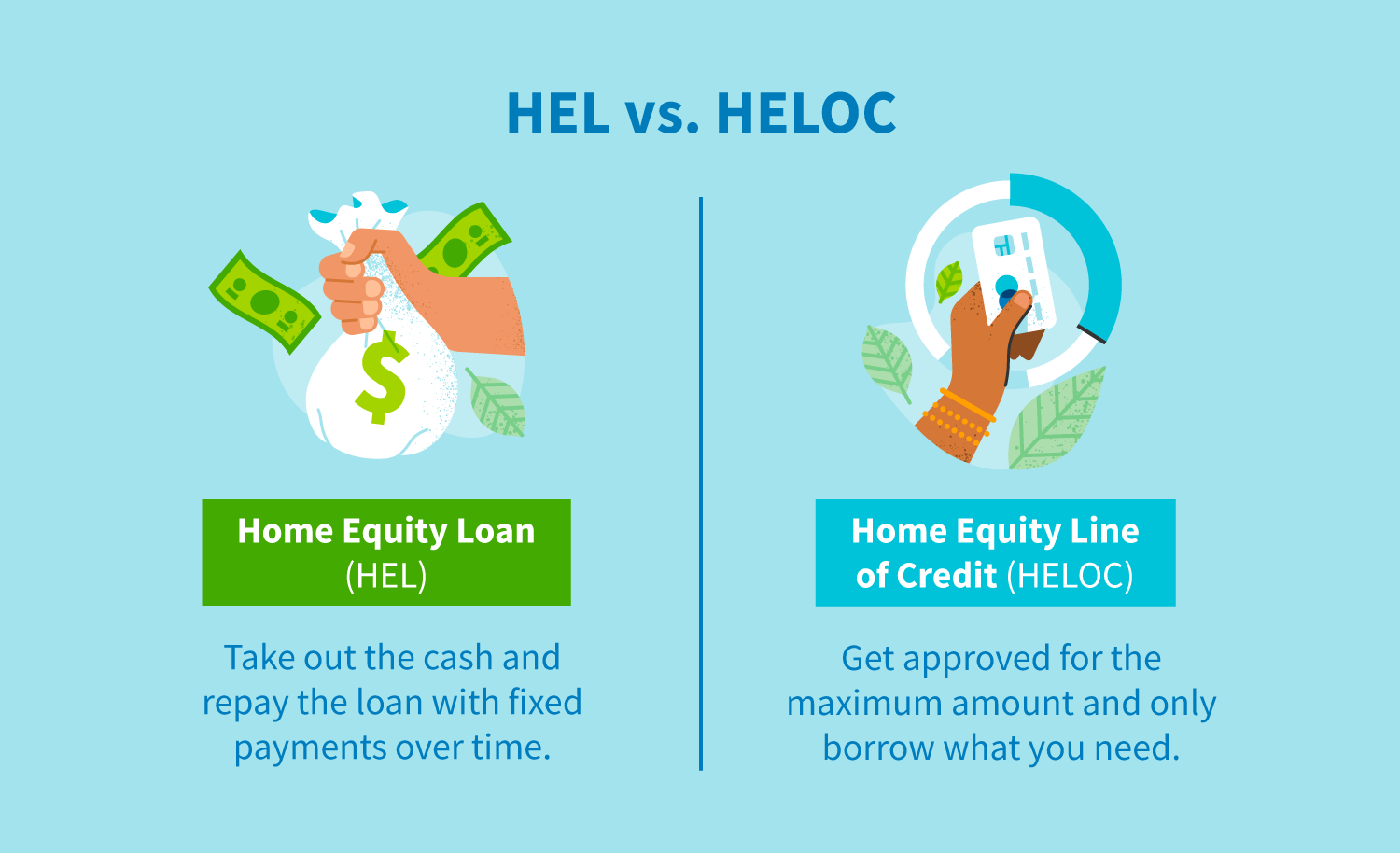

A HELOC is a flexible line of credit that allows you to borrow against the equity in your home. You can draw funds as needed, up to a pre-approved limit. It’s similar to a credit card, where you only pay interest on the amount you borrow.

A Home Equity Loan, on the other hand, provides a lump sum disbursement upfront. You repay the loan with fixed monthly payments over a set term, similar to a traditional mortgage.

Why Consider a HELOC?

- Flexibility: Borrow as needed, repay as you wish.

- Potential Tax Benefits: Interest paid on a HELOC may be tax-deductible.

- Home Improvement Financing: Fund renovations or upgrades to increase your home’s value.

- Debt Consolidation: Consolidate high-interest debt into a lower-interest HELOC.

- Investment Opportunities: Use the funds to invest in real estate or other ventures.

Key Differences between HELOCs and Home Equity Loans

| Feature | HELOC | Home Equity Loan |

| Flexibility | Flexible borrowing, draw funds as needed | Lump sum disbursement |

| Interest Rate | Variable interest rate | Fixed interest rate |

| Repayment | Repay as you borrow | Fixed monthly payments |

HELOCs for Rental Property Owners

If you own a rental property, a HELOC can be a valuable tool:

- Renovation Financing: Fund necessary repairs or upgrades to attract tenants.

- Cash Flow Management: Cover unexpected expenses or bridge gaps in rental income.

- Investment Opportunities: Use the funds to purchase additional properties or invest in real estate ventures.

Important Considerations:

- Risk: Remember, a HELOC is secured by your home. Defaulting on the loan could lead to foreclosure.

- Eligibility: Because HELOCs are primarily restricted to primary residences, you will want to open one up while you are living there, or if you plan on converting it into a rental property, applying for one before moving out

- Interest Rates: Be aware of variable interest rates, which can fluctuate over time.

- Consult a Financial Advisor: Before taking out a HELOC, consult with a financial advisor to assess your financial situation and determine if it’s the right choice.

By understanding the nuances of HELOCs and home equity loans, you can make informed decisions to leverage your home equity and achieve your financial goals.